By Randy Smith,

Mobile Wallet Media

June 19, 2013

About Mobile Wallet Media

Mobile Wallet Media is a news media, analyst, marketing and consulting firm focused on the future of mobile: payments, marketing, loyalty commerce, security, prepaid, virtual currency, daily deals and the convergence of them all with social and local. The Chief Editor, Randy Smith, was the primary founder, inventor and former CEO of MobilePayUSA, a TechCrunch Disrupt Startup Alley Winner.

Media Partners

Discussing the Future

of Mobile Commerce!

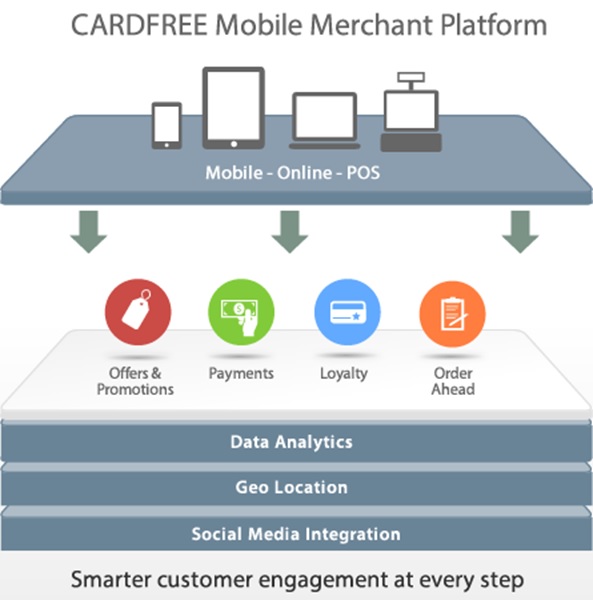

If you have not taken notice yet of CARDFREE yet, you should. Though CARDFREE has yet to get out of the gate with a customer deployment, they certainly have assembled a team that is perhaps unmatched in the industry. The CARDFREE team is largely responsible for the most successful mobile payment apps in use today; Starbucks Card Mobile and the Dunkin Donuts app while the teams were at mFoundry, Corfire and Starbucks. The company has also received US $10 million in funding to help fuel it's launch.

Jon Squire, CEO of CARDFREE, was SVP of Wallet & Payments at mfoundry for three years before a two year reign as CMO of the mobile commerce solution CorFire. Chuck Davidson, who conceived, led and launched the Starbucks Card Mobile scheme, leads product for CARDFREE. Jeffrey Katz, who is an investor and chairman of the board at CARDFREE, is also known for founding Mercury Payments Systems. Other lead executives also hale from mFoundry, InComm and Visa. The Starbucks Card Mobile app and Dunkin Donuts apps alone combine for a vast majority of mobile transactions taking place in the US market today. Starbucks recently shared they are processing 4.5 million transactions per week!

A recent article by Berg Insight declared that Starbucks Card Mobile App is dominating mobile payments right now in capturing most of the 500 million of the in-store mobile payment transactions. But such dominance by retailer payment apps may prove to be short lived as the report also pointed out that by 2017, universal mobile wallets will drive the majority of the in-store purchase volume, which they estimate to be near US $44 billion by 2017.

Last week at the 6th Mobile Commerce Payment Innovations Summit I had a chance to sit down for interview with Darren Beyer, Head of Platform for CARDFREE.

Q: Tell me about the CARDFREE platform?

Darren: We’re incorporating a whole host of different features and functions; loyalty, offers, rewards, stored value, etc. into one combined platform . . . Having everything together tightly coupled gives you a lot more flexibility to meet individual client needs, but beyond that the economics make a lot more sense. It’s one of things that has been a detriment to existing mobile platforms today. They have been talking with legacy platforms for stored value. If I have a plastic card, maybe I check the balance once and then use to buy lunch. So I’ve spent a dime. With mobile it’s very different. Before I transact, every time, we need to show the balance. Then I transact there’s another hit. Potentially there’s another balance inquiry. In the end it may cost 3-4 times what it does in the physical world. And that’s just stored value, you also have offer and loyalty platforms. Because we can do that we take the economics out of the decision tree. We end up becoming a more favorable economic piece of the equation.

Our SuperCommerce Series

Search, Social or SuperCommerce?

The key to commerce shall be the seamless completion of the value and convenience chain for consumers and merchants alike.

How may Google, Facebook and First Data disrupt Daily Deals? Will EVOLUTION lead

to REVOLUTION? How about M&A?

Daily Deals Manifest Destiny

Can one live on deals alone?

Tour D' Mobile Payments

PayPal, Google Wallet, ISIS, Square & more. What are the barriers to adoption and how they may be overcome?

AUG

SEPT

SEPT

The Future of Money

Where will payments be in 2020? Will mobile over take cards & cash? Learn how a 'Secure, Social & Rewarding' wallet will disrupt it all?

Bridging the POS GAP

NFC is Tortoise and the 2D Bar Code is the

hare. Retailers, simplify the myriad of choices!

Learn how DISRUPTION is RIPE for 2013!

OCT

OCT

Greed is NOT GOOD!

Cause Commerce IS!

Cause Commerce can set you apart! Learn what it is, why it will soon be, non-optional, and how it will add to your Social Brand.

NOV

Loyalty LIKE Never Before!

The convergence of Social & Rewards is here!

Learn how Top of Mind & Automation will rule! Maximize, Mobilize & Unify Ads & ROI!

NOV

Companies and leaders, to remain relevant and profitable, must embrace innovation or risk becoming irrelevant or extinct.

Top 5 Killers of Innovation!

HDTV - High Def. Total Vision Where are your Blind Spots?

Connect the dots! See the big picture!

If your Mobile Strategy is unclear, you may be

missing key pieces. Get a holistic perspective.

AUG

DEC

TM

New Series for 2013

The 'Disruptive Innovation Meteor' named MOBILE has struck the world's of retail payments, banking and marketing. Firms wanting to survive, compete and win in this new environment must adapt by embracing disruptive innovation or risk becoming irrelevant or extinct. Read story

IF YOU FORGOT WHAT INNOVATION LOOKS LIKE

WATCH IPHONE'S FIRST COMMERCIAL BELOW . . .

Disruptive Innovation and Dysfunctional Dinosaurs

image source: abcnews.go.com

Use discount code “WALLET” to receive $200 off registration.

Copyright 2012. All rights reserved, Mobile Wallet Media, Inc. News & Opinion on the Future of Mobile Payments & Commerce!

Sponsor Spotlight Coming Soon! >>

CARDFREE’s Mobile Payment & Loyalty Platform will be Mobile POS Agnostic