By Randy Smith,

Mobile Wallet Media

May 21, 2014

About Mobile Wallet Media

Mobile Wallet Media is a news media, analyst, marketing and consulting firm focused on the future of mobile: payments, marketing, loyalty commerce, security, prepaid, virtual currency, daily deals and the convergence of them all with social and local. The Chief Editor, Randy Smith, was the primary founder, inventor and former CEO of MobilePayUSA, a TechCrunch Disrupt Startup Alley Winner.

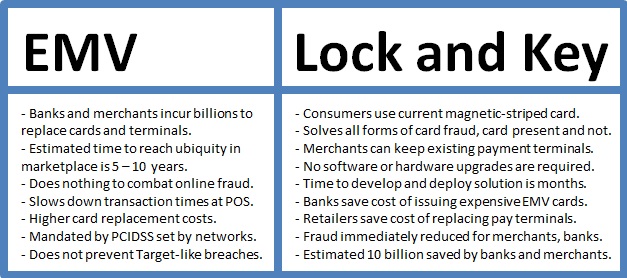

The Target breach was a recent catalyst in igniting the fraud solutions war pitting EMV vs. ‘Lock and Key.’ EMV you know, but Lock and Key? As covered in my prior article Ondot Systems and TSYS both recently announced they are offering a service enabling consumers to use a mobile phone app to lock and unlock or set parameters for card usage by proximity, one-time use and more.

The EMV PCI mandate that was outdated the second it was enacted. It is also a ‘Mafia-styled offer not to be refused’ due to the liability transfer to merchants that fail to adopt EMV. PCI mandates are not fun play dates unless you are a payment terminal manufacturer and essentially are the main reason why EMV is being pushed so hard. The terminal pushers have come up with some new reason to replace terminals every few years since they first rolled out. Up until EMV most all the features added were worthy of upgrade or at least had rationality to back them up.

EMV enthusiasts will say EMV is long overdue in the U.S., but it is estimated to cost banks and merchants near 10-billion for this EMV makeover. What will be gained from this overhaul that is not estimated to be ubiquitous for another 5-10 years? Slower transactions, higher card replacement costs for banks and still online fraud is not solved.

Even if EMV terminals were deployed at Target stores it would not have stopped the breach. The breach was made through a vendor access portal. Hackers from there gained access to payment terminals. PCI rules did not require card credentials to be encrypted inside terminals but only in transit. Several years back the Heartland breach revealed hackers were capturing card data in transmission to processors from POS. It appears a reactionary response to preventing card fraud has been PCI policy. EMV does not solve the card fraud problem. Until we reach EMV ubiquity we’ll still be stuck with magnetic stripes on cards.

A banking executive shared that Ondot Systems cut fraud losses by sixty percent. This is some serious savings for banks. Banks need only to integrate with TSYS or Ondot Systems and announce service to their customers. No new terminals for merchants or cards for consumers like with EMV. No billions of dollars and billions of hours spent or perhaps wasted. Calculating in fraud loss reduction and lower ongoing costs for banks to be able to continue to issue the conventional mag-stripe card, makes Lock and Key even more attractive.

Media Partners

Discussing the Future

of Mobile Commerce!

Our SuperCommerce Series

Search, Social or SuperCommerce?

The key to commerce shall be the seamless completion of the value and convenience chain for consumers and merchants alike.

How may Google, Facebook and First Data disrupt Daily Deals? Will EVOLUTION lead

to REVOLUTION? How about M&A?

Daily Deals Manifest Destiny

Can one live on deals alone?

Tour D' Mobile Payments

PayPal, Google Wallet, ISIS, Square & more. What are the barriers to adoption and how they may be overcome?

AUG

SEPT

SEPT

The Future of Money

Where will payments be in 2020? Will mobile over take cards & cash? Learn how a 'Secure, Social & Rewarding' wallet will disrupt it all?

Bridging the POS GAP

NFC is Tortoise and the 2D Bar Code is the

hare. Retailers, simplify the myriad of choices!

Learn how DISRUPTION is RIPE for 2013!

OCT

OCT

Greed is NOT GOOD!

Cause Commerce IS!

Cause Commerce can set you apart! Learn what it is, why it will soon be, non-optional, and how it will add to your Social Brand.

NOV

Loyalty LIKE Never Before!

The convergence of Social & Rewards is here!

Learn how Top of Mind & Automation will rule! Maximize, Mobilize & Unify Ads & ROI!

NOV

Companies and leaders, to remain relevant and profitable, must embrace innovation or risk becoming irrelevant or extinct.

Top 5 Killers of Innovation!

HDTV - High Def. Total Vision Where are your Blind Spots?

Connect the dots! See the big picture!

If your Mobile Strategy is unclear, you may be

missing key pieces. Get a holistic perspective.

AUG

DEC

TM

2013 Series

The 'Disruptive Innovation Meteor' named MOBILE has struck the world's of retail payments, banking and marketing. Firms wanting to survive, compete and win in this new environment must adapt by embracing disruptive innovation or risk becoming irrelevant or extinct. Read story

IF YOU FORGOT WHAT INNOVATION LOOKS LIKE

WATCH IPHONE'S FIRST COMMERCIAL BELOW . . .

Disruptive Innovation and Dysfunctional Dinosaurs

image source: abcnews.go.com

Copyright 2012. All rights reserved, Mobile Wallet Media, Inc. News & Opinion on the Future of Mobile Payments & Commerce!

Sponsor Spotlight Coming Soon! >>

The Card Fraud Solutions War Has Begun: Could 'Lock and Key' Derail EMV?

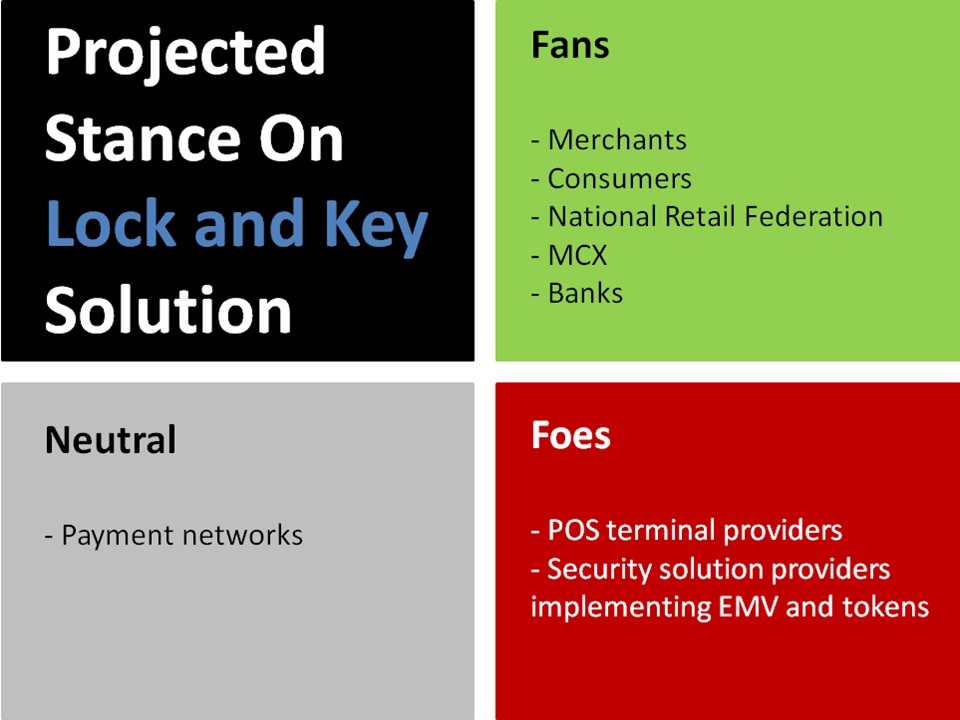

In weighing the scale of Lock and Key vs. EMV the scales lean to Lock and Key. So the question of the day is should the PCI EMV mandate be repealed in favor of Lock and Key?

To be sure merchants, consumers and banks will favor this solution over EMV. It seems the only reason left to keep the EMV mandate in place is sales of payment terminals. NFC HCE for mobile payments may still be another reason for merchants to replace terminals. BLE and beacon and QR code solutions may however derail the need for NFC in terminals. Besides can’t an NFC peripheral just be plugged in rather than replace terminals?

San Francisco, June 10-11