By Randy Smith,

Mobile Wallet Media

September 9, 2013

About Mobile Wallet Media

Mobile Wallet Media is a news media, analyst, marketing and consulting firm focused on the future of mobile: payments, marketing, loyalty commerce, security, prepaid, virtual currency, daily deals and the convergence of them all with social and local. The Chief Editor, Randy Smith, was the primary founder, inventor and former CEO of MobilePayUSA, a TechCrunch Disrupt Startup Alley Winner.

Media Partners

PayPal has taken a big step in the right direction with its new mobile payment app. The previous design was straight out of 2003 (yes, I'm aware apps did not exist until 2008). However, for a mobile wallet to have a fighting chance it needs to provide more convenience and security than the physical wallet.

2012 - SuperCommerce Series

Search, Social or SuperCommerce?

The key to commerce shall be the seamless completion of the value and convenience chain for consumers and merchants alike.

How may Google, Facebook and First Data disrupt Daily Deals? Will EVOLUTION lead

to REVOLUTION? How about M&A?

Daily Deals Manifest Destiny

Can one live on deals alone?

Tour D' Mobile Payments

PayPal, Google Wallet, ISIS, Square & more. What are the barriers to adoption and how they may be overcome?

AUG

SEPT

SEPT

The Future of Money

Where will payments be in 2020? Will mobile over take cards & cash? Learn how a 'Secure, Social & Rewarding' wallet will disrupt it all?

Bridging the POS GAP

NFC is Tortoise and the 2D Bar Code is the

hare. Retailers, simplify the myriad of choices!

Learn how DISRUPTION is RIPE for 2013!

OCT

OCT

Greed is NOT GOOD!

Cause Commerce IS!

Cause Commerce can set you apart! Learn what it is, why it will soon be, non-optional, and how it will add to your Social Brand.

NOV

Loyalty LIKE Never Before!

The convergence of Social & Rewards is here!

Learn how Top of Mind & Automation will rule! Maximize, Mobilize & Unify Ads & ROI!

NOV

Companies and leaders, to remain relevant and profitable, must embrace innovation or risk becoming irrelevant or extinct.

Top 5 Killers of Innovation!

HDTV - High Def. Total Vision Where are your Blind Spots?

Connect the dots! See the big picture!

If your Mobile Strategy is unclear, you may be

missing key pieces. Get a holistic perspective.

AUG

DEC

TM

New Series for 2013

The 'Disruptive Innovation Meteor' named MOBILE has struck the world's of retail payments, banking and marketing. Firms wanting to survive, compete and win in this new environment must adapt by embracing disruptive innovation or risk becoming irrelevant or extinct. Read story

IF YOU FORGOT WHAT INNOVATION LOOKS LIKE

WATCH IPHONE'S FIRST COMMERCIAL BELOW . . .

Disruptive Innovation and Dysfunctional Dinosaurs

image source: abcnews.go.com

Copyright 2012. All rights reserved, Mobile Wallet Media, Inc. News & Opinion on the Future of Mobile Payments & Commerce!

Sponsor Spotlight Coming Soon! >>

PayPal's Mobile Payment App Looks Good, But Where's Loyalty, Gift, Scalability & Security?

Enter code MWMDISC for 10% off (thru July 26)

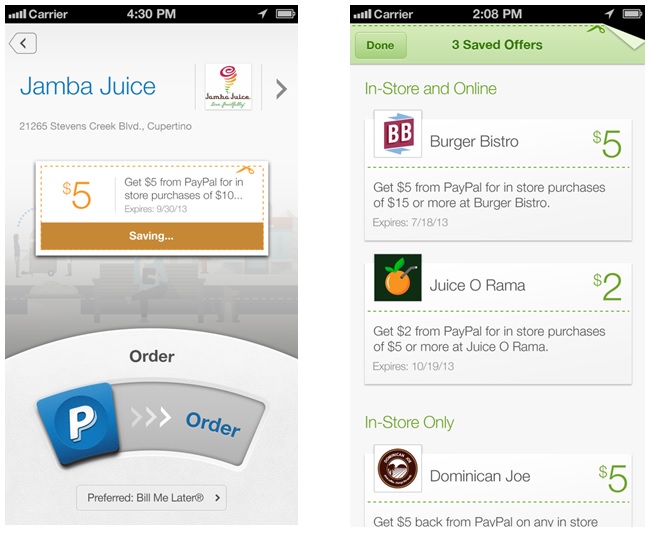

With a new bold focus on shopping in the real, local world, PayPal is trying to extend its reach from being just an ecommerce and P2P payment company. The ability to save offers and redeem them seamlessly with payment is what shoppers want. Being able to pay at table and order in advance at restaurants adds value as well. Paying friends in seconds to settle a bill is a nice complimentary feature. This being said, these new conveniences shall not often persuade me to use their app unless I can use it all over town, not just at small boutiques. And where's the loyalty and gift card program, enhanced security and scalability?

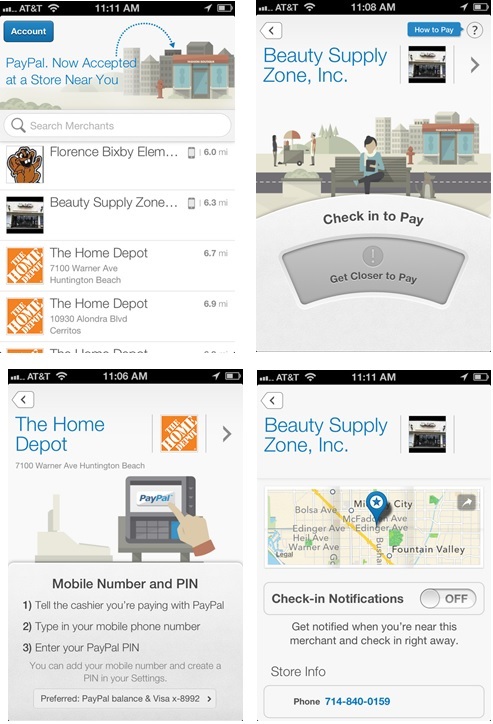

Yes, we are back to the chicken and egg issue here of scalable technology to enable in-store mobile payments. For now it appears PayPal is sticking to their current mobile POS tech of geo-fencing and checking in to pay. But is this scalable? While this revamped app looks better on the surface, it is still stuck with the same problems I pointed out last fall. Their check-in service is limited to merchants using tablets and thieves may capture your phone number and pin and use to make fraudulent purchases.

Now to be fair and forward-looking, PayPal may have already solved the security problem with entering your phone number and static PIN (my idea is they can solve this problem through one-time use, in-app dynamic PIN generation). And in regards to scalability of their check-in to pay beyond tablets, they recently partnered with Micros, NCR and Mercury. So they appear be moving to expand their check-in to pay service. But, question is how user friendly will this service be for cashiers in navigating such transactions? If there are 15 people in line or in-store, checked in and ready to pay, like with Pay With Square, does the cashier have to sift through images to find the correct person to charge the transaction to?

Last year I ventured out to pay at Home Depot using PayPal, I was able to only after the cashier got assistance from a manager that knew how to navigate their POS software to process PayPal. And I was unable to find a local merchant that knew how to process payments using PayPal Check-In (went to one and called 2-3 others). I found out that just because a merchant has signed up for PayPal, it does not mean they have trained employees on how to use their services.

I'm still kind of baffled here. Why is PayPal stuck in 2008-2011? Are they not a leader in emerging payments? It's not for lack of capital! So what gives? Oh yeah speaking of giving, where's 'Cause Marketing?' And where’s ‘Social Sharing’? What's the delay here? PayPal has a partnership with Discover and there are other more scalable ways to accelerate their acceptance in market PayPal's Check-In. PayPal needs to check pride at the door (as do all mobile wallet players) and embrace innovation that will propel them forward lest they will be passed by Apple, MCX, LevelUp, Facebook and others. PayPal, I love your reach and progress, but you must step up your game. It's time to hold no punches!